50/30/20 Rule for Loan Borrowers

Manikaran Credit & Leasing Co. Pvt. Ltd

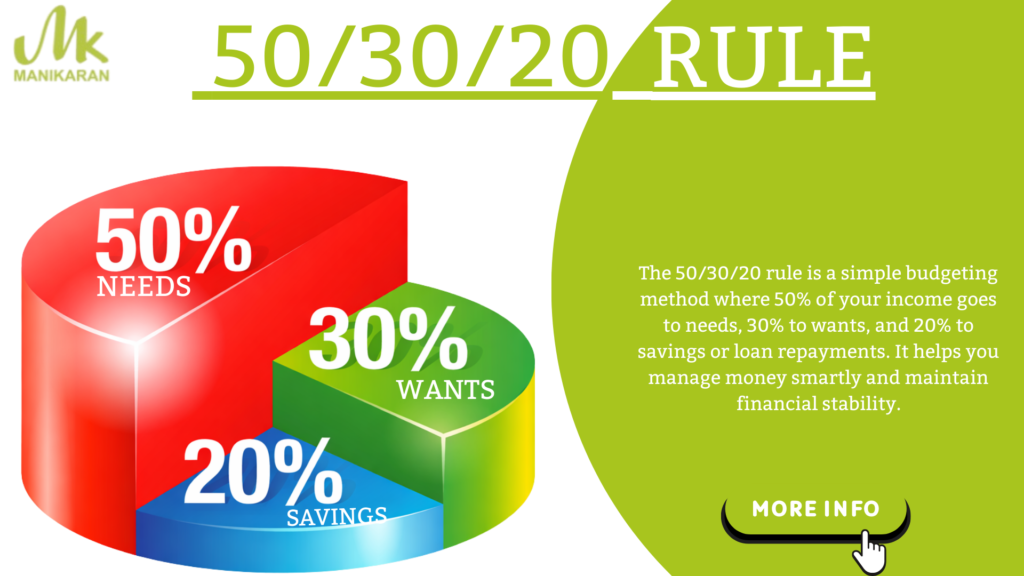

50% – Needs

50% – Needs  30% – Wants

30% – Wants 20% – Savings &

20% – Savings & You don’t overborrow Your EMI is manageable You avoid EMI bounce charges You have an acceptable CIBIL score You avoid loan stressYou only borrow what you can afford. Improves Loan Approval Reduces EMI

You don’t overborrow Your EMI is manageable You avoid EMI bounce charges You have an acceptable CIBIL score You avoid loan stressYou only borrow what you can afford. Improves Loan Approval Reduces EMI Protects Your C

Protects Your C Maintains

Maintains Taking a loan based on maximum eligibility Ignoring monthly cash flow Not maintaining Emergency Fund ???? Reliance on credit cards for EMI services Во-первых, имеем несколько личных Remember: It does not matter whether NBFC sanctions an amount of ₹5 lakhs or not, you should not take an amount of ₹

Taking a loan based on maximum eligibility Ignoring monthly cash flow Not maintaining Emergency Fund ???? Reliance on credit cards for EMI services Во-первых, имеем несколько личных Remember: It does not matter whether NBFC sanctions an amount of ₹5 lakhs or not, you should not take an amount of ₹